Taking the turnoff to commercial

Brokers are turning once-daunting commercial deals into everyday work, helped by non-bank appetite, SMSF strategies and more familiar digital lodgement processes

More

FOR YEARS, commercial deals sat at the far edge of many brokers’ mental map, like the industrial estate at the outskirts of town that everyone drives past but rarely turns into. Residential files filled the in-trays, the systems were familiar, and the idea of longer leases, complex cash flows and lengthy application forms belonged in a different postcode.

Now the traffic patterns are changing. Business owners want predictable reviews and cash flow, they are willing to pledge commercial property or self-managed super fund balances to secure it, and they are asking the same brokers who helped them into their homes to help them fund their warehouses, offices and shopfronts.

In broker groups and lender BDM meetings, the language of offsets, online lodgement, serviceability calculators and equity release is creeping into conversations that would once have stopped at the family home. Commercial is starting to look less like a specialist detour and more like a natural extension of the advisory route many brokers already know how to drive.

Commercial lending is moving from sideline to staple for residentially focused mortgage brokers, as shifting borrower priorities, non-bank appetite and more familiar submission processes make it easier to structure, lodge and manage these loans with confidence. But what’s driving demand, where do brokers find opportunities in areas such as SME funding and SMSF property, and how can small changes to process and mindset turn commercial from ‘too hard’ into an everyday part of the business?

Despite growing participation, something still holds brokers back from treating commercial as core business. But it’s not education – what continues to limit deeper engagement is a fear of the unknown. “Commercial lending can feel complex, especially for brokers who are unsure about the process, the nuances involved, or who to engage with to successfully structure and settle a deal,” Stuart says.

Chesworth agrees. “There’s often the perception that the leap to commercial lending is a bridge too far, given the paper-heavy application process with 15-page application forms, different serviceability terminology and comprehensive valuations.”

Bluestone is unlocking the next wave of growth in opening commercial property-backed lending to residential brokers, he says. “We’ve added commercial security to the Bluestone products they’re familiar with. Lodgement is exactly what they’re already used to through ApplyOnline, with e-signed customer declarations and acknowledgements and simple upload of documents in its secure environment, removing the need for email attachments and the risk of security breaches. Plus, we use the same servicing terminology of Net Servicing Ratios.”

Bannister says La Trobe Financial has focused on eliminating misconceptions and operational obstacles to ensure accessibility within commercial lending. “We don’t impose excessive accreditation requirements; a single application form applies to all products,” he says. His firm’s business development managers have expertise in both commercial and residential lending, and a dedicated team of in-house commercial credit analysts ensures that submissions are reviewed directly by key decision-makers.

Stabilising construction costs and rising house prices have led to notable improvements in developer feasibility, which will be a tailwind for the sector. “We have strong conviction that the demand for property finance will accelerate significantly over the next one to two years, aided by the pressing need to address a national housing supply shortage, which is expected to be placed under further pressure as immigration levels continue to run at over 200,000 people per annum,” Bannister says.

A growing population requires more than just housing, he says. “There will be increasing demand for retail, office and industrial premises, and we’re excited about the opportunities this will present.”

“SMEs will continue to be our core focus,” Stuart says. “They represent the backbone of the commercial economy, yet a significant portion of this market remains underserved. Industry estimates suggest 70% of commercial lending continues to flow to the major banks, and while that works well for some borrowers, it leaves roughly 30% of the market dealing with more complexity or non-standard circumstances.”

This is the segment MA Money is particularly keen to support: business owners who may be misunderstood or overlooked despite having fundamentally sound propositions, Stuart says. The firm offers a more nuanced approach to income assessment, ABN tenure, prior credit events and loan purposes such as cashout, all of which can be critical for growing businesses that don’t fit neatly into traditional lending frameworks.

Bannister sees opportunity at the other end of the size spectrum. “La Trobe Financial offers one of the broadest product suites in the market, with each product able to be customised to meet the specific needs of borrowers, providing a unique level of flexibility,” he says. “Combine that with a set-and-forget approach and loan sizes up to $50 million, La Trobe Financial is among few lenders capable of supporting blue-chip commercial property owners with substantial financing needs.”

A key factor influencing credit demand right now is the pressing need to address a national housing supply shortage. “This has resulted in strong growth in loan volumes for our construction, site acquisition and residual stock loan products. We have a strong ongoing appetite to continue to finance the housing formation,” Bannister says.

One of the most common pressure points in adviser-introduced commercial deals is treating them too similarly to residential transactions. “For example, seeking approval at a maximum LVR with little more than a property address doesn’t provide enough context for a meaningful credit assessment in a commercial environment,” Stuart says.

In commercial lending, decisions around security acceptance, loan size and LVR are highly detail-driven, he says. To improve approval certainty and long-term results for their clients, brokers need to invest more time up front in understanding the full client picture. “That means getting clear on the client’s objectives, financial position and risk profile, and presenting a well-rounded, fully considered submission. In commercial lending, deeper upfront discovery isn’t just helpful; it’s essential to achieving the right outcome.”

Homeownership is a fundamental part of the Australian dream. However, the path can be challenging, especially when traditional lending can be strict and unforgiving. We’re here to change that. Since 2000, Bluestone Home Loans has been helping borrowers with complex or unique financial situations access the market with confidence, offering them a chance to purchase property – when others won’t – by providing tailored lending solutions. We empower brokers to serve a broader range of clients, from self-employed professionals to borrowers with past credit issues or those seeking niche lending options. With a 25-year legacy, Bluestone Home Loans has become a trusted leader in the Australian lending market, known for delivering innovative, flexible and straightforward solutions that break the mould of traditional lending.

In Partnership with

“A consistent trend observed among commercial borrowers is their preference for stable financial products without ongoing review clauses, as well as their desire to work with dependable and consistent lenders,” says Cory Bannister, senior vice president and chief lending officer at La Trobe Financial.

With interest rates rising in February and forecasts pointing to further increases in 2026, borrowers holding facilities subject to regular reviews may face challenges, according to Bannister. “This environment may create opportunities for us and for brokers, as clients seek alternative options for financing their commercial properties.”

The pattern isn’t limited to refinancing. “One of the strongest themes we’re seeing is the strategic use of equity,” says Craig Stuart, head of commercial at MA Money. “Brokers are bringing us clients who are releasing equity to consolidate existing debt, manage ATO obligations or reposition their businesses for the next phase of growth.”

Rather than taking on additional unsecured debt, many business owners are prioritising cash flow certainty and balance sheet resilience, Stuart says. Another development is the rise in commercial purchases through SMSFs, particularly for owner-occupied premises. “Business owners are increasingly choosing to leverage their superannuation position rather than drawing on operating cash flow, allowing them to secure premises they control while building a long-term portfolio within their super structure,” Stuart says.

Richard Chesworth, head of specialised distribution at Bluestone, says the firm is seeing growth from its existing customer profiles and from new commercial clients being introduced through fresh adviser relationships. “What’s resonating is the flexibility we can offer compared to traditional banks, like a fully functioning offset sub-account with true netting of monthly interest, which keeps things simple for customers.”

SMSF commercial lending goes beyond the product itself, Chesworth says. “Brokers often work closely with customers and their brokers to structure lending in a way that supports broader family asset decisions, including reallocation through an SMSF where appropriate.”

Share

Cory Bannister

La Trobe Financial

Industry experts

Craig Stuart is head of commercial at non-bank lender MA Money, responsible for its commercial lending portfolio, including SMSF commercial loans. With almost 30 years’ experience in the mortgage industry, primarily within the non-bank sector, Stuart brings deep expertise across credit and sales. He has held senior national roles and is known for building strong broker relationships and delivering practical, tailored lending solutions. At MA Money, Stuart focuses on a clear credit process, consistent support and helping brokers deliver effective outcomes for their commercial clients.

MA Money

Craig Stuart

Cory Bannister is senior vice president and chief lending officer at La Trobe Financial. Bannister has over 20 years’ experience in financial services and has held a number of positions across credit and distribution since joining the business in 2000. As CLO, Bannister is focused on managing substantial wholesale and retail investors. He holds diplomas in mortgage lending and business accounting and resides in Melbourne.

La Trobe Financial

Cory Bannister

Stuart says many lenders are now using platforms such as NextGen and CitoPlus for loan application lodgement, which has materially improved service levels, turnaround times and the overall adviser experience. Improvements in commercial property data are also making a tangible difference. “Access to more comprehensive information, including sales history, recent imagery and floor plans, is enabling lenders to make better-informed decisions up front. For brokers and borrowers alike, this translates to clearer expectations, faster feedback and more reliable outcomes across the life of a commercial deal,” says Stuart.

Where non-banks have an edge�The gap between the economics of bank and non-bank offerings has narrowed, and brokers are increasingly turning to non-bank providers for what are bankable scenarios to prioritise speed, flexibility and service. “Compared to traditional banks, non-banks can often provide more flexible terms and can often move in a more agile manner, which can be crucial for businesses needing access to capital,” Bannister says.

Non-bank and specialist lenders bring a distinct advantage to commercial lending, particularly when it comes to supporting SMEs with more complex or non-traditional circumstances. The key advantages of non-bank lenders include speed to decision, streamlined documentation and a willingness to take a more holistic view of a business’s current and historical performance. “This open-minded approach can be particularly valuable for SMEs that don’t fit neatly into traditional bank credit frameworks,” Stuart says.

More commercial customers are choosing to work through brokers instead of going direct to traditional banks. “Bluestone offers both full-doc and alt-doc application options, so brokers can move quickly rather than waiting on full financials,” Chesworth says. “Add to that a simple 30-year loan term with no set reviews and the flexibility of an offset account, and brokers can deliver a streamlined experience.”

Brokers keep full ownership of the relationship, he says. “Using the same servicing calculator and ApplyOnline process they rely on today helps make the transition seamless. And when it comes to SMSF commercial lending, non-banks are essential. Banks stepped away from this space almost a decade ago, but it remains a significant part of SMSF borrowing needs.”

“Compared to traditional banks, non-banks can often provide more flexible terms and ... move in a more agile manner, which can be crucial for businesses needing access to capital”

CORY BANNISTER, �LA TROBE FINANCIAL

Making the process feel familiar

Technology is starting to close the gap between how brokers lodge residential applications and the way they approach commercial ones. “Residential lending has moved quickly towards electronic lodgement and document upload, but commercial lending hasn’t followed at the same pace,” Chesworth says. “Many lenders still rely on long paper forms and email attachments, which adds time and security risk.”

Bluestone has addressed this by allowing brokers to lodge commercial loans electronically through ApplyOnline, just like they do with residential. “Brokers tell us it’s a game changer because it keeps things simple, secure and consistent,” Chesworth says.

Others agree that clear adviser notes make a world of difference. “When an application explains the customer’s situation and the broader transaction, it can result in a much faster response and, in many cases, faster approval,” says Chesworth. “On the other hand, sparse notes usually lead to extra questions or rework, which can slow things down.”

Bannister puts it simply. “Engaging your BDM as early as possible will dramatically shift your and your client’s experience,” he says. “We have BDMs expertly versed in commercial lending, which means they’re able to give confident responses on credit appetite, policy and requirements that can help brokers reduce the time to yes and increase their conversions.”

“There’s often the perception that�the leap to commercial lending is a bridge too far, given the paper-heavy application process with 15-page application forms, different serviceability terminology and comprehensive valuations”

RICHARD CHESWORTH, BLUESTONE HOME LOANS

A shift in borrower priorities

The fear factor

Published 09 Mar 2026

Craig Stuart

MA Money

La Trobe Financial is Australia’s premier alternative asset manager and a proven and trusted investment partner for institutional and retail investors, with c. A$20 billion in assets under management. We believe that property and homeownership are the foundation of wealth creation and achieving financial independence. This is why we have created our broad product range offering lending solutions to suit your needs at every life stage, from buying your first home through to building your business and maximising your SMSF and retirement income.

Find out more

Despite the push towards automation and efficiency, there’s agreement that commercial lending will always require a manual lens. “Every transaction is different, and judgement remains critical,” Stuart says. “The opportunity lies in replicating some of the efficiency gains achieved in the residential channel, without losing the nuance that commercial deals demand.”

Bannister puts it plainly: “There’s no doubt that technology will continue to reshape our industry, but it’s the nuance of the human-based decision-making at La Trobe Financial that gives brokers confidence that their hard work in structuring a complex submission isn’t overlooked. We continue to deploy human capital to uplift our tech and make existing in the La Trobe Financial ecosystem easier. But fundamentally, and what is unlikely to ever change, is that we’re a business that is assisted by technology and not defined by it.”

Chesworth says the commercial space is only at the start of its digital transition. “The sooner technology is embraced, the better the experience will be for brokers and customers alike.”

As the map keeps redrawing itself, the old industrial estate at the edge of town is starting to look less intimidating. Brokers who once stayed in the residential suburbs are already taking the turnoff, often with the same systems, credit partners and client relationships they use every day.

For borrowers, this evolution means fewer surprises, more control and someone they already trust in the passenger seat. For brokers willing to venture off the main thoroughfare, commercial is just a different stretch of road that’s becoming part of the same network, and the signs pointing towards growth are getting harder to ignore.

What slows deals down

Who’s being underserved

Where growth is coming from

The human element

Richard Chesworth

Bluestone Home Loans

As head of specialised distribution at Bluestone, Richard Chesworth brings more than 20 years of experience in commercial and SMSF lending strategies, giving brokers practical guidance to help navigate complex client needs. He works closely with advisers, brokers and industry partners to structure lending solutions that balance flexibility with clear, straightforward execution.

Bluestone Home Loans

Richard Chesworth

MA Money is one of Australia’s fastest-growing non-bank lenders, with over $5 billion in loans under management. Working in partnership with mortgage brokers, MA Money offers a broad range of lending solutions across residential, commercial, bridging, SMSF, vacant land, expat and non-resident property loans, including support for self-employed and non-traditional-income clients. With flexible credit assessment, responsive service and streamlined processes, MA Money helps brokers move quickly and solve more complex scenarios. The focus is on certainty, speed and practical solutions that support brokers in delivering for their clients.

Find out more

“Industry estimates suggest 70% of commercial lending continues to flow to the major banks … [That] leaves roughly 30% of the market dealing with more complexity or non-standard circumstances”

CRAIG STUART, MA MONEY

Find out more

Advertising

Authors

E-newsletter

Contact Us

Contact Us

Australian Mortgage Awards

Events

White papers

Webinar

Australian Broker Podcast

Resources

TV

Virtual Roundtable

Sector Focus

Power Panel

Partnership Profile

Independent Feature

Executive Team Profile

Exclusive Leader Profile

Business Update

Big Deal

Premium Content

Technology

Reverse Mortgages

Spotlight Series

Specialist Lending

SME

Investment Loans

Commercial

Speciality

Best In Mortgage

News

News

RSS

Sitemap

About us

Conditions of Use

Cookie Policy

Privacy policy

Terms & conditions

People

Firms

Copyright © 2026 KM Business Information Australia Pty Ltd

Source: MFAA Industry Intelligence Service, 19th Edition, 1 April 2024–30 September 2024 �

Number of mortgage brokers also writing commercial loans

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

Apr 21-Sep 21

Oct 21-Mar 22

Apr 22-Sep 22

Oct 22-Mar 23

Apr 23-Sep 23

5,268

5,396

6,118

5,864

5,654

Oct 23-Mar 24

Apr 24-Sep 24

6,755

7,023

28.8%

29.0%

31.8%

30.1%

28.5%

30.7%

31.5%

Show proportion of all brokers

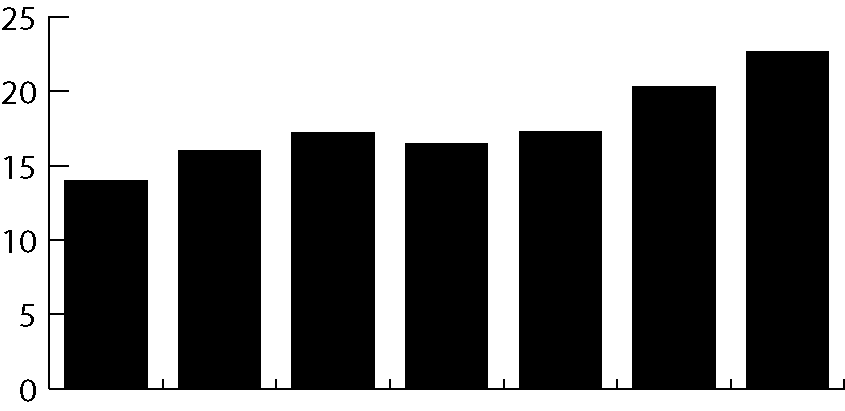

Source: MFAA Industry Intelligence Service, 19th Edition, 1 April 2024–30 September 2024 �

$bn

25

20

15

10

5

0

Apr 21-Sep 21

Oct 21-Mar 22

Apr 22-Sep 22

Oct 22-Mar 23

Apr 23-Sep 23

Oct 23-Mar 24

Apr 24-Sep 24

$14.0bn

$16.0bn

$17.24bn

$16.50bn

$17.29bn

$20.31bn

$22.69bn

$2.54m

$2.96m

$2.82m

$2.81m

$3.06m

$3.01m

$3.23m

Show average value per broker

Value of commercial lending�settled by mortgage brokers